May, 2024 – The last two years have been a whirlwind of market turmoil in 2022 followed by a remarkable recovery in 2023. By the end of 2023 we were just right back where we started at the beginning of 2022. So far in 2024, growth stocks have been leading the way. Artificial intelligence (AI) is certainly the buzzword of the decade thus far, and more lifechanging advancements(?) are on the way.

No one is really talking about quantum computing yet, but this promises to be just as big—if not bigger, if you can believe it—than artificial intelligence. At some point, these two monolithic human feats of science will meet, and the results will be truly monumental. Even unimaginable.

In the meantime, what has not changed is human nature. And, of course, government meddling.

We are excited about the future of our technology, but deeply concerned about our fiscal irresponsibility. Our national debt (the debt we admit) has now passed $34 trillion and there is no end in sight to the spending. New spending bills are always coming out, and this often leads to newly minted money in the system, making our inflation even worse. In the meantime, everyone is waiting for inflation to come down so that the Fed will cut rates. Yet, Congress continues to spend.

Besides our public debt, which is like living on the slopes of Mt. Vesuvius, some more immediate issues are showing ominous signs. We have several concerns that we are monitoring currently, and they don’t bode well for stocks in the near future:

- Leading Economic Indicators

- Higher Interest Rates

- Corporate Debt

- Stock Valuations

- Unwinding Fed Balance Sheet

- Commercial Office Space

There are three types of economic indicators: leading, lagging, and coincident. Coincident lets us know how things are currently going. Lagging tells us how things have gone. And you guessed it, Leading helps to tell us about what’s coming. It is easy to tell where we are and where we’ve been, but not so easy to tell where we’re headed. Leading indicators can (somewhat) do that.

Think about a neighborhood that is planned for the next year or two. What is the first thing you have to do to build a neighborhood? Architectural plans, zoning, land acquisition, orders for delivery of concrete, lumber, masonry, lighting. Interviewing and hiring of new staff and salespeople, et cetera. I’m sure you can think of many more. Notice how each of these things hints of a new neighborhood to come when not one person has put a spade in the ground.

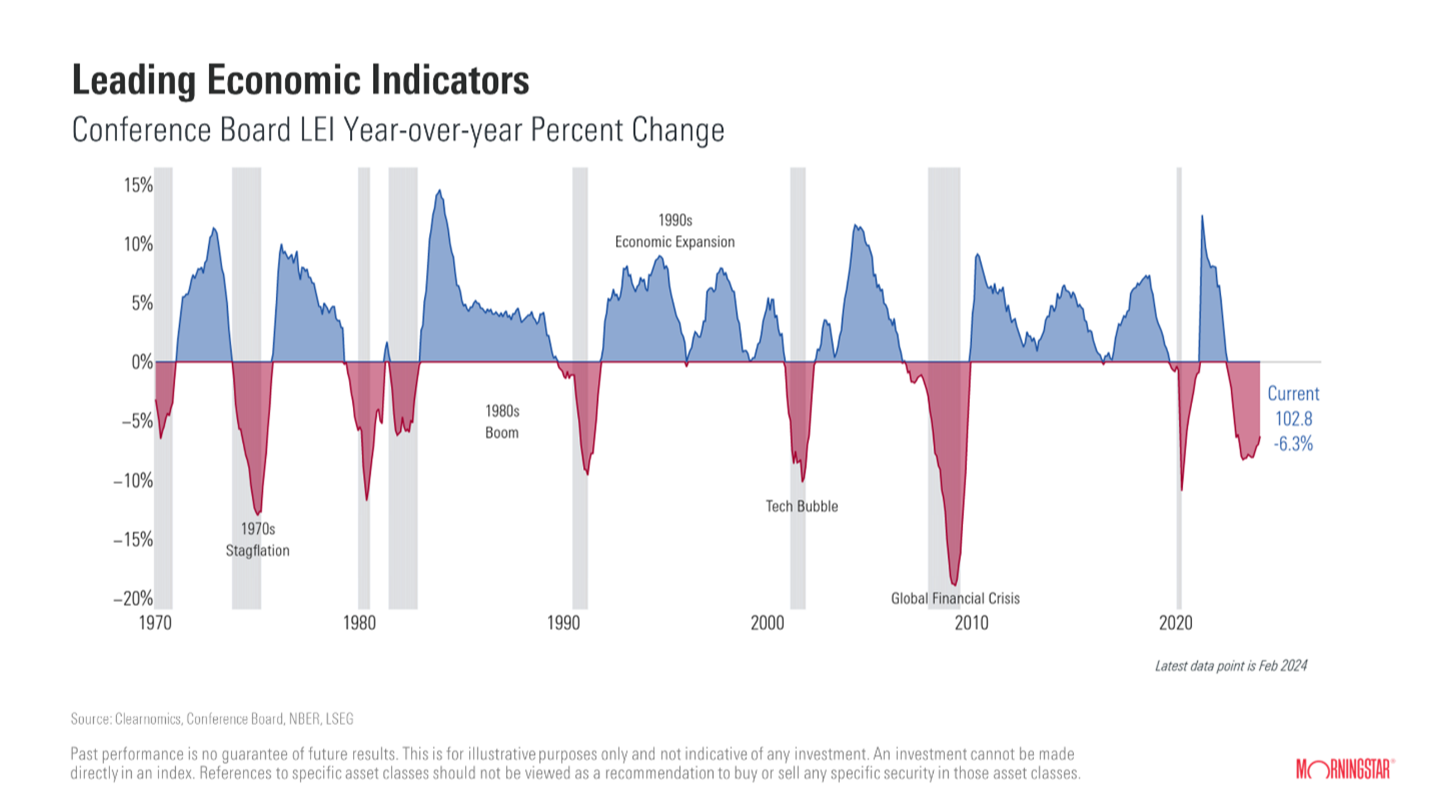

Well, there are several indicators like this that economists look to for guidance on where the economy is headed. The chart below shows leading indicators since 1970. The grey vertical lines indicate recessions. Note that in every single instance where leading indicators break below 5%, a recession follows, ushered in by a significant market correction.

Note that our current number is -6.3%. In the last 52 years, there has been a recession 100% of the time when we were similarly situated.

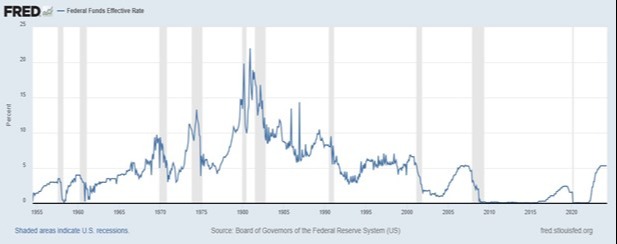

One of the most significant variables in determining a possible coming recession is interest rates. The cycle goes like this: Coming out of a recession, the Fed lowers rates and injects stimulus—they call it expanding the balance sheet, buying treasuries, quantitative easing, or anything but creating new money, which is really what it is. New money raises all boats, but eventually creates inflation, and artificially low interest rates create a misallocation of assets. Then, the Fed starts raising interest rates to fight inflation. Eventually, historically, the market crashes and a recession ensues.

The chart above shows the Fed Funds rate since 1955. Note that in most cases rates peak out, sometimes plateau, but then sharply reverse. Next comes a grey vertical line. Those grey lines indicate recessions—recessions ushered in by market crashes. The cycle is so obvious that it’s predictable. (Thank you Ludwig von Misesi).

If you look and see where we are now—rates are higher than they’ve been in 24 years. They have recently plateaued, and everyone is waiting with bated breath for a drop in rates, often promised, as yet delivered. With new government spending constantly being injected into the economy, inflation is unlikely to reverse any time soon, which means rates are likely to be higher for longer.

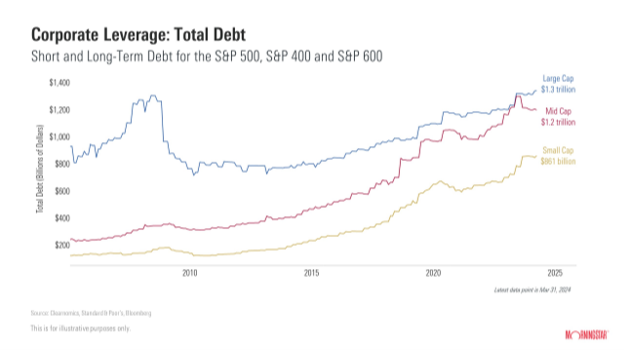

This is especially bad for those with a lot of debt—like US companies. The chart below illustrates the amount of corporate debt currently on the books. You can see that the large cap debt (blue line) is back to pre-2008 levels while Mid Cap (red line) and Small Cap (gold line) companies have taken on more than ever.

The companies took on all this debt back when interest rates were near zero, and for the most part they are still enjoying those low rates. But as the weeks march on, those lower-rate bonds are maturing, and they are being refinanced into new, higher-rate issues. Higher debt service cuts right into the bottom line. This is one reason the market wants lower rates.

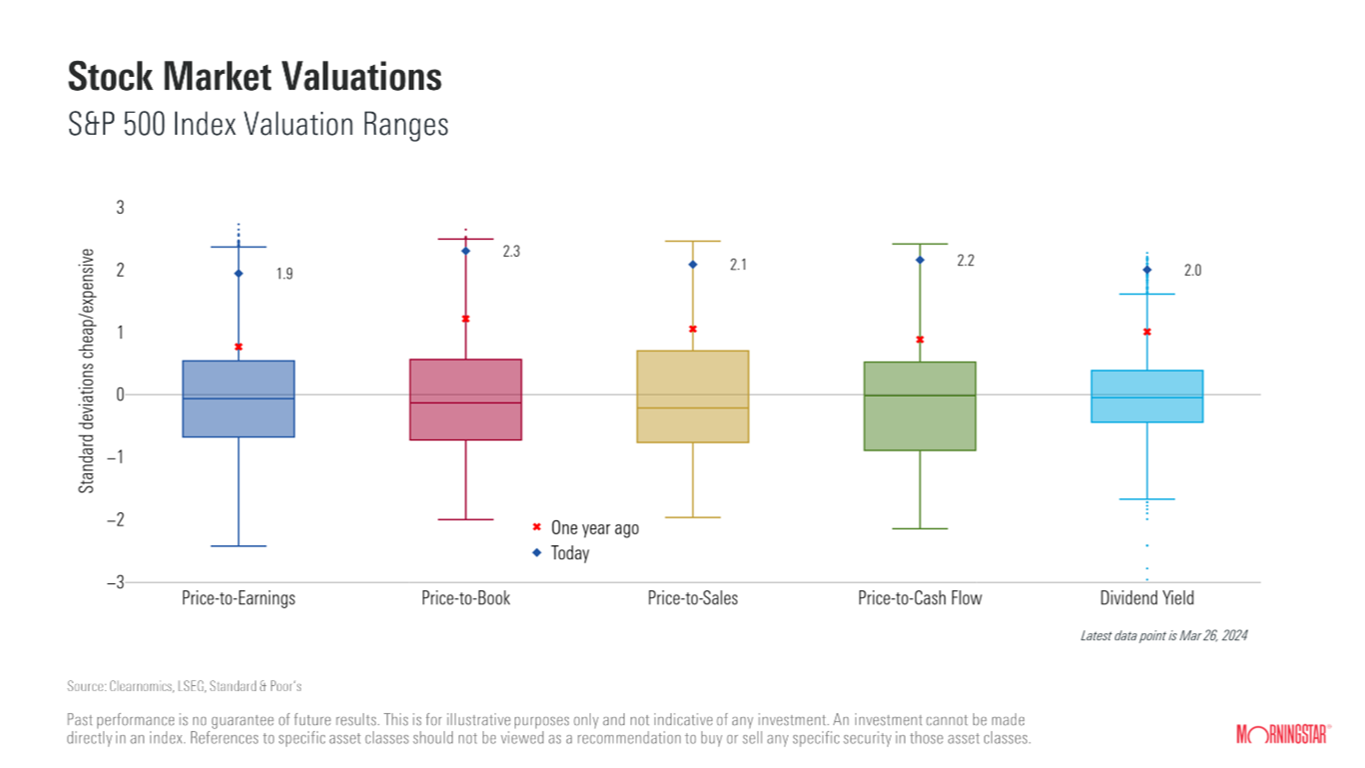

Speaking of bottom lines, corporate earnings (net of all those expenses like taxes and interest) is one of the most significant factors in a stock’s price, the so-called Price/Earnings ratio. There are other factors that economists look at when determining a reasonable value of stocks, such as Price-to-Book, Price to Sales, Price to Cash Flow, and Dividend Yield.

The chart below illustrates the historical ranges of each of these factors in the shaded boxes. The red dots are the S&P 500 valuations from one year ago (March, 2023) as compared to this year (March 26, 2024), the blue dots. Notice that in every single instance, the valuations from last year were above the historical range. More alarmingly, look at the blue dots, the recent valuations. No matter how you slice it, stocks are about two deviations above their historical range.

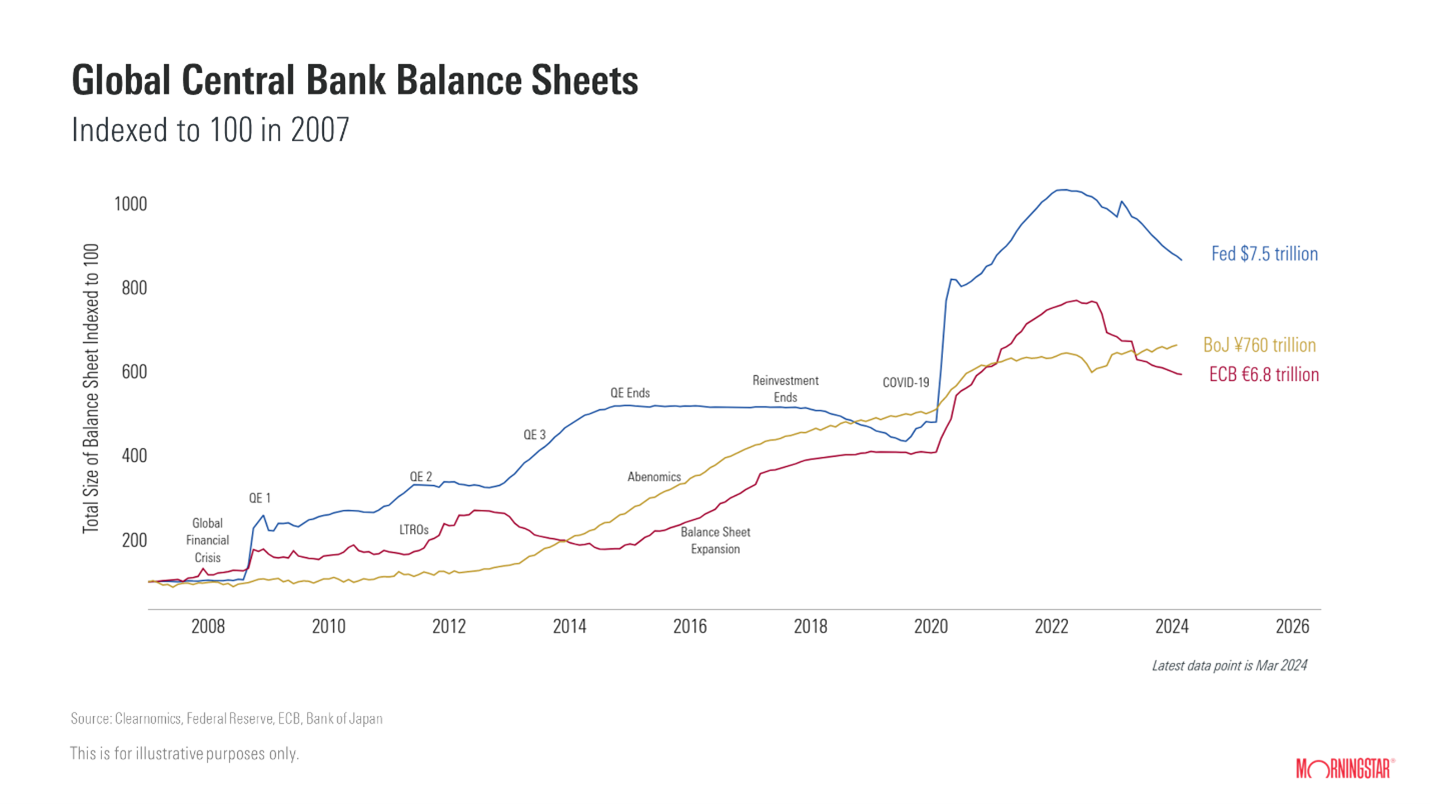

As if all this weren’t enough, we have another major factor to consider, which is the unwinding of the central banks’ balance sheets. This is a little more difficult to get your brain around but think of it as money creation and money destruction—electronically.

During Covid, the Fed created an additional $7 trillion which made its way out into the economy quite rapidly, thus creating all the inflation we’re currently enjoying. Now, the central banks are unwinding that process—as they should—but history has shown that it is never pretty. Eventually there is less money in a system that has adjusted for more money and a “credit event” occurs, ushering in a potential market downturn.

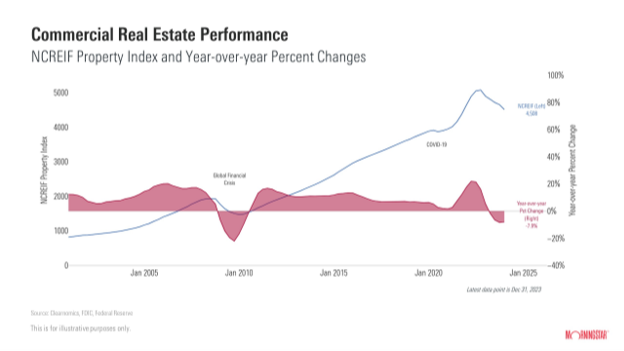

And speaking of a market downturn, we can already see one occurring in commercial real estate. Office space has not recovered from Covid, and many companies are finding (or believe) that they don’t need all that extra office space, and it certainly cuts down on the commutes, which is better for everybody. Well, everybody except office landlords, and the banks that finance them. The landlords have been crushed by the vacancies, and we believe it is only the beginning. Many leases are still on the books, but a significant amount will be rolling off this year. Others will simply default.

In fact, as recently as April 18, 2024, a new report published by real estate data provider ATTOM revealed that “there were 625 commercial real estate foreclosures in March, up 6% from February and 117% from the same time last year. California had the highest number of commercial foreclosures in March, with 187 properties. While that marked an 8% decrease from the previous month, it is a stunning 405% jump from the previous year.”ii We believe the commercial office space sector is in for real trouble—triggering more mid-sized bank failures.

Economies as big as ours do not turn on a dime—it took a couple of years for inflation to show itself after the Covid printing spree, and it will take a while longer to get it under control. In the meantime, stock market/interest rate correlations continue to be a reality, and in every instance I have mentioned above, we can see this cycle repeating again.

If it were just one indicator or maybe another, we could possibly look past it. But when you stack them all together, the reasoning for our caution becomes apparent. We are looking forward to getting it over and done, because we are excited about our shopping list that we have on deck—just waiting for the right time, and price—when all these indicators have reversed.

I get the oft repeated question of “when will the market crash?” And all I can tell you is that history says about 9-14 months AFTER the Fed pauses rate hikes. The Fed paused last September. See my letter from December 2023 “The Tail of the Dragon”iii for a more detailed analysis of this.

In any event, if you have questions or concerns, or would like to chat about your positioning in case of a market downturn, please contact us to schedule a call or meeting.

As always, we very much appreciate having you as a client and a member of our family and look forward to seeing you at one of our upcoming events!

My very best,

J. Kevin Meaders, J.D. CFP, ChFC, CLU

The views and opinions are those of J. Kevin Meaders, J.D., CFP®, ChFC, CLU and should not be construed as individual investment advice, nor the opinions/views of Cetera Advisor Networks. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Additional risks are associated with international investing such as, currency fluctuation, political and economic stability, and differences in accounting standards. Due to volatility within the markets mentioned, options are subject to change without notice.

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Dow Jones Industrial Average, Dow Jones, or simply the Dow, is a price-weighted measurement stock market index of 30 prominent companies listed on stock exchanges in the United States. The Nasdaq Composite is a stock market index that includes almost all stocks listed on the Nasdaq stock exchange. The Nasdaq Composite is a stock market index that includes almost all stocks listed on the Nasdaq stock exchange.

Securities and advisory services are offered through Cetera Advisor Networks LLC, member FINRA/SIPC, a broker-dealer and registered investment adviser. Cetera is under separate ownership from any other named entity.

Estate services offered by Magellan Legal, LLC and tax services offered by Magellan Tax, LLC. Estate and tax services offered separately from Cetera Advisor Networks LLC, which does not provide legal or tax advice.

__________________________________________________________________________________________________

i https://mises.org/profile/ludwig-von-mises

ii https://www.foxbusiness.com/economy/commercial-real-estate-foreclosures-jumped-march-trouble-looms

iii //static.fmgsuite.com/media/documents/b7078abd-7f93-4697-b6fb-6a491f38e3e7.pdf