June, 2026 — If you didn’t know where the Strait of Hormuz was before this year, then you certainly know now. (Funny how world conflict can teach us a lot about geography—sad that that’s what it takes.) You’ve also no doubt heard that some 25% of the world’s seaborne oil trade transits the Strait, making it one of the world’s largest strangleholds.[i] And indeed, we have seen how complete it can be.

On this side of the pond, things seemingly could not be better. The Dow, Nasdaq, and S&P 500 are all hovering near their all-time market highs, and AI is all one hears about. (As someone who watches a lot of documentaries, I’m already sick of AI. Can’t they change the voice now and again?)

In any event, it doesn’t take an economist to see that there is a serious disconnect between what’s going on in the rest of the world and what’s going on here at home. Granted, the US has been relatively shielded from the effects of the Strait’s closure because we simply do not import that much from the region. With Venezuela coming back online, one would expect that we would import even less.

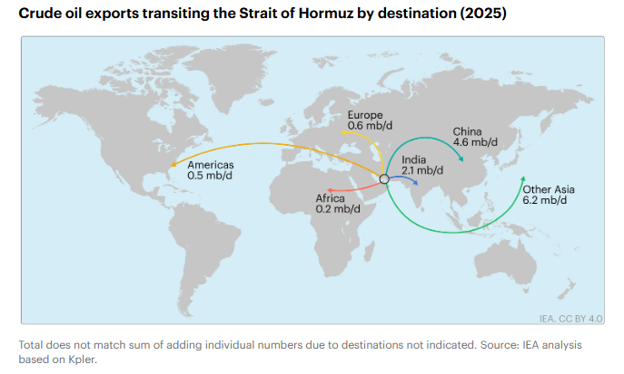

Based on information provided by the IEA, the entire Americas received less than 500,000 barrels per day from the Strait in 2025, as compared to China with 4.5 million and other Asian countries accounting for 6.2 million. For us, not such a big problem; for them, a real problem, especially the longer this blockage extends. (Though hopefully now it’s over).

I suspect this is one of the reasons the Trump administration has been in no real hurry to reopen the Strait by force—if such a thing can be done. As the thinking goes, the longer the crisis persists, the more injury to our Communist friends in the East. As a side benefit though (whether contemplated or not), keeping Iran’s hands tied so to speak minimizes the assistance they can provide Putin in his war of aggression against Ukraine.

Nonetheless, at least one firm has noticed the disconnect between the Strait’s extended closure and current stock valuations. HFI Research, who focuses on the oil and natural gas sector, is warning that:

Much of the [stock] rally has been fueled by hope that a peace deal is just around the corner, though that optimism looks misplaced, HFI suggested. The situation resembles that of the oil shock in 1973, HFI added, the year that anoil crisis sparked a 48% peak-to-trough decline in the S&P 500, Costello said. The index didn't recover those losses for about seven years. "Sustained high oil prices act as a tax on a slowing economy, and sudden price spikes become more likely, pressuring both the economy and stock prices. The market has priced in none of this, which leaves it dangerously exposed to a severe decline," Costello wrote in a client note on Wednesday.[ii]

Of course, during the oil shock of 1973, we didn’t have AI or the soaring profits that investors have become accustomed to as they buy every dip, regardless of the circumstances. Remember that old saying about when every bet’s a winner?

Without a doubt AI is here to stay, and it has truly been remarkable—just as the internet has been. The lesser-known miracle right around the corner is quantum computing, which promises to be bigger than AI and the Internet, if you can imagine. Quantum computing utilizes particle entanglement—which Einstein called “spooky action at a distance.” We don’t understand it, but hey, it works like a charm every time.

But even with great inventions like these, which truly do offer profound potential for all of humanity, market cycles cannot be avoided forever. And truly, the technology and communications sectors have been boosting the overall stock market for some time.

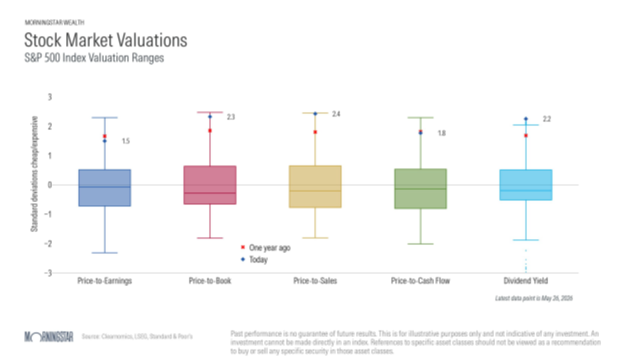

The ongoing concern, as I have cautioned ad nauseum, is the extremely high stock valuations vis-à-vis historic valuations with respect to several different indicators: Price-to-earnings, price-to-book value, price-to-sales, price-to-cash flow, and dividend yield.

The following chart—which you have no doubt seen before—provides a helpful illustrative view of stock market valuations in each of these categories.

The colored boxes above indicate the twenty-year average—or the mean—of each category. The blue dots indicate where we are today (as of May 26, 2026) and the red dots indicate where we were one year ago.

The blue dot on the second indicator, for instance, price-to-book value, is currently at 2.3 times its 20-year average. In the world of statistics, a standard bell curve (normal distribution) contains about 99% of all data within 2.5 standard deviations. A deviation of 2.3 times is very high, placing it roughly in the top 1% to 2% of all data points.

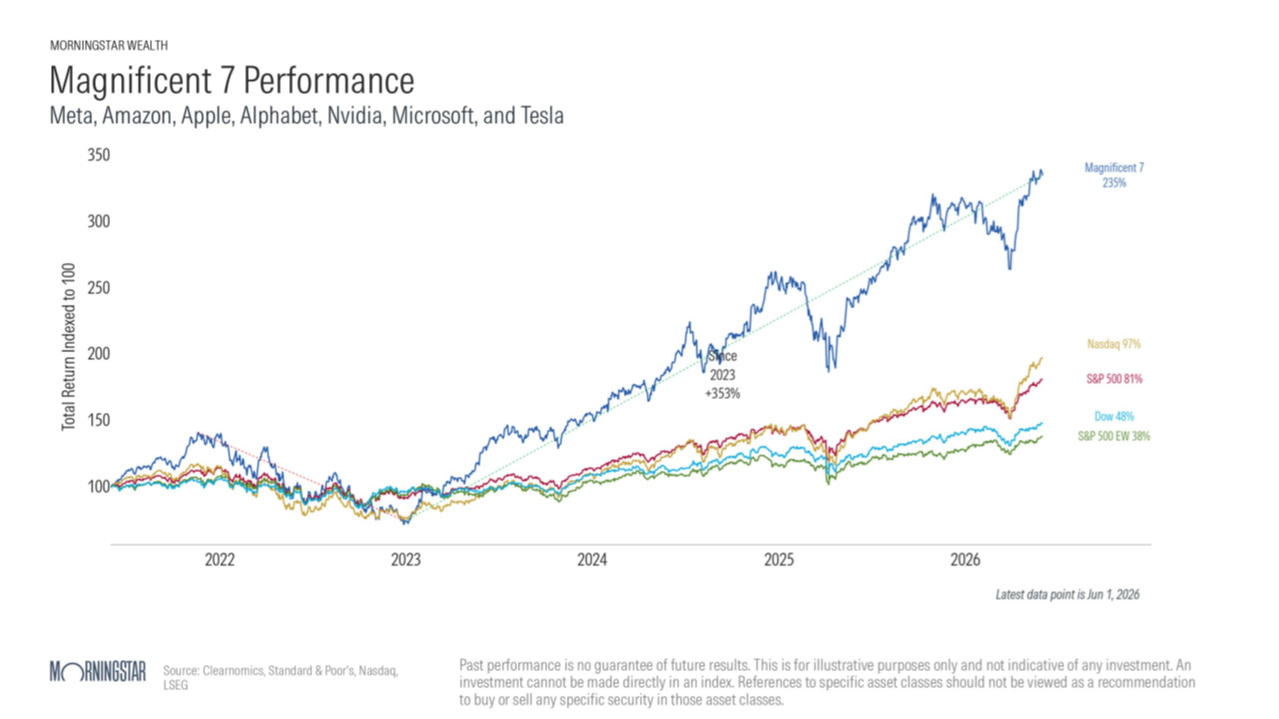

All that being so, it really hasn’t mattered much. With every dip, investors pile into the Mag 7 without as much as a second thought about any of it.

The thinking is that no matter what the numbers say, AI-related stocks will go ever higher.

That sort of thinking only works if you completely ignore history and human nature, which you can, for a time—perhaps an extended time. What’s that old saying about “this time it’s different?" In 1999, even I started to believe it. But these scientific revolutions come around every so often: the wheel, bronze, the chariot, the crossbow, the plow, the compass, the printing press, the steam engine, the telegraph, the telephone, the combustion engine, the airplane, the computer, the internet, artificial intelligence, and quantum computing. I’m sure you can think of some I’ve forgotten.

The point is that it does not matter what “it” was then or what “it” is now or what “it” will be in the future, market cycles always come around again eventually, and history is all we have to reasonably determine what happens next.

If you look at each category in the chart above again, you can see that we are very near or above 2 deviations in each one except price-to-earnings. However, if we look at a rolling 10-year price-to-earnings ratio using inflation-adjusted earnings, we see a more worrisome trend.

Invented by Robert Shiller, this indicator has been flashing red. Going back all the way to 1920, we have seen the ratio this high only twice before—once in 1929 and again in 1999. I don’t need to remind you of what happened next.

Forward to today, the Strait of Hormuz has been closed since February, and now, finally, it will reopen? So they sign a deal, but no matter how much Trump tries to rely on Iran’s good faith word to make a deal regarding their uranium, they will never give it up.

The deal gives Iran 60 days to begin “pre-implementation discussions.” This is just more of the same delay tactics they’ve been using forever. They know midterm elections are coming up in November, and the Republicans are likely to lose the House and Senate again. If the Iranians agree to give up their enriched uranium, they’re lying, and we’re right back where we were during the Obama years—useless UN inspections of distraction sites.

The Islamic regime is still in place, and at the end of the day, nothing has really changed. First and second string are dead, and perhaps a more hot-headed third string is in power now. And still there are many others waiting in line.

All in all, despite the incredible resiliency of our stock markets through the tariff tantrum, Venezuelian police action, and now the Iranian conflict, one has to wonder how long our luck can run. Operation Cuban Freedom is up next, if Trump can get it going before the midterms. Investors don’t have time to digest one event before we’re on to the next.

If you look at insider trading (which they are required to disclose to the SEC), insiders know that a correction is surely due, so in the meantime every company (and insider) that can off-load risk right now is certainly looking at their options. One option is to sell off shares to the uneducated public in a massive IPO before prices can correct.

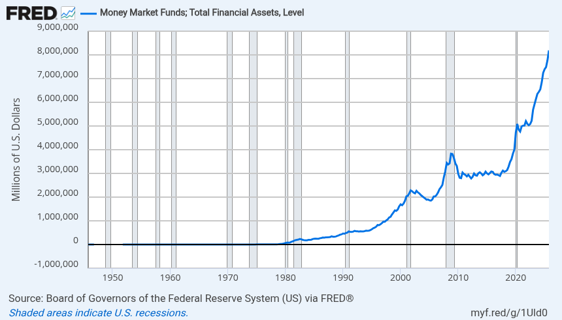

There is plenty of cash on the sidelines just chomping at the bit to be deployed, too. Look at this chart of the total amount sitting in money market funds. Over $8 trillion! And this does not include the trillions sitting in short-term treasuries.

Remember the Covid pandemic? The Fed created a fresh $7 trillion dollars that the Treasury distributed in PPP and other slush contrivances. Remember that? Remember what happened to grocery prices and home prices and everything else? That’s called inflation, and it has been devastating main street—though Wall Street, as usual, probably knows but doesn’t care.

So ask yourself this question: What would happen to our economy if most of that $8 trillion were deployed? Invested, spent, loaned, whatever. Would that create more inflation? You bet it would! It would throw gas on an already raging fire.

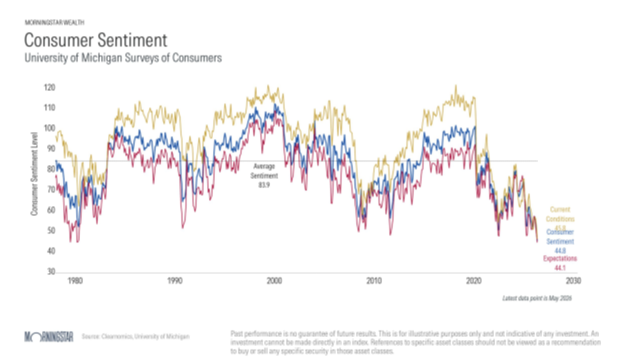

Corporate insiders may be fat and happy, but the rest of our society is suffering. You may not see it in the Upper East Side, Martha’s Vineyard, John’s Creek, Georgia, Lincoln Park, Illinois, or Pacific Heights, California or any of the other ritzy neighborhoods in America, but the working classes are struggling. Inflation has hit lower and middle income households hard, and consumer sentiment reflects the large percentage of our population who have seen their standard of living decrease.

The University of Michigan’s “latest consumer sentiment score is 44.8 — the lowest since the survey began in 1952. That means more people are saying they are struggling financially right now, or worry that they will be in the future, than they did during the COVID-19 pandemic, the Great Recession in 2008 and in the days following 9/11.”[iii]

Now take into consideration that nearly 70% of the US’s GDP is driven by consumer spending, and you can see why this might be a concern for the retail and service industries, and indeed the broader economy. People spend less when they feel strapped.

As you can see, there are a lot of moving parts and very little clarity. The most important thing right now is to be aware of these inherent dangers but also be alert to any opportunities that might arise. Flexibility is paramount, and its important to have plans in place no matter what circumstances arise: An eye on the future, but grounded in the past.

If you are concerned or need some reassurance about our plans, then I encourage you to reach out to me at kevin@magellanplanning.com or 404-257-8811. I’d love to hear from you and look forward to meeting with you soon.

We’ve got some exciting new systems coming soon that we look forward to sharing with you, including advanced estate and financial planning software, tax efficiency software, a personal client hub with an encrypted documents vault, the ability to amalgamate all your assets in one place, and our own app to access your accounts and financial plans.

I also look forward to seeing you at one of our upcoming social events.

Stay well, and enjoy your summer.

My very best,

J. Kevin Meaders, J.D. CFP®, ChFC, CLU

The views and opinions are those of J. Kevin Meaders, J.D., CFP®, ChFC, CLU and should not be construed as individual investment advice, nor the opinions/views of Magellan Planning Group, Inc. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Additional risks are associated with international investing such as currency fluctuation, political and economic stability, and differences in accounting standards. Due to volatility within the markets mentioned, options are subject to change without notice.

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Dow Jones Industrial Average, Dow Jones, or simply the Dow, is a price-weighted measurement stock market index of 30 prominent companies listed on stock exchanges in the United States. The Nasdaq Composite is a stock market index that includes almost all stocks listed on the Nasdaq stock exchange. The Nasdaq Composite is a stock market index that includes almost all stocks listed on the Nasdaq stock exchange.

Magellan Planning Group, Inc is a SEC Registered Investment Advisor. Estate services offered by Magellan Legal, LLC and tax services offered by Magellan Tax, LLC.

The return and principal value of bonds fluctuate with changes in market conditions and interest rates. If bonds are not held to maturity, they may be worth more or less than their original value.

[ii] https://www.businessinsider.com/stock-market-correction-oil-price-shock-bond-yields-iran-war-2026-6

[iii] https://www.cbsnews.com/minnesota/news/what-is-us-consumer-sentiment/