September, 2025 – Today is a big day. Today—September 17, 2025 —the Federal Reserve finds out if it still has control over the U.S. economy, particularly the $58 trillion bond market.

The Fed just lowered rates by another quarter point (25 basis points) to 4 percent. Everyone has been waiting to see what would happen to bond yields. Would they follow the Fed lead and drop, or would they rebel like they did last September, and spike?

Yesterday, in anticipation of a rate cut, bond yields were down slightly. Today, just after the expected cut—they are pretty flat. But yields should be dropping, and bond prices rising.

It’s certainly a relief that bond yields didn’t spike—which would mean that bond prices fell. And they have some, but not nearly the 9 percent drop we saw last year. And it wasn’t just the US, but Europe, Japan and Great Britain. What does this tell us? It is saying the global bond market is fed up with all the debt. There’s just no more appetite for government debt anywhere in the world.

So, we (the US as dictated by the Federal Reserve) have decided that we are not going with austerity, we’re going with inflation. There are only two choices. Here is a quote from Ludwig von Mises, written in 1951, that could have been written yesterday:

This country, and with it most of the Western world, is presently going through a period of inflation and credit expansion. As the quantity of money in circulation and deposits … increases, there prevails a general tendency for the prices of commodities and services to rise. Business is booming.

Yet such a boom, artificially engineered by monetary and credit expansion, cannot last forever. It must come to an end sooner or later. For paper money and bank deposits are not a proper substitute for nonexisting capital goods. Economic theory has demonstrated in an irrefutable way that a prosperity created by an expansionist monetary and credit policy is illusory and must end in a slump, an economic crisis. It has happened again and again in the past, and it will happen in the future, too.

There is no way around it. We have to choose between ending the credit expansion (austerity) and causing a bust, or continuing the money creation and making inflation worse and worse, ultimately destroying our currency. We have chosen the latter.

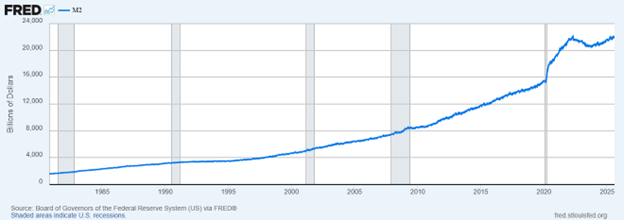

The chart below shows all the money out there sloshing around in our economy, which is just a bit over $22 trillion. This is the very definition of inflation—which is the more units in existence the less the value of each unit. Very simple.

You can see the big jump there during Covid when the Fed injected a freshly made $7 trillion into the system. Then you can see a peak and what looks like a small dip. But ultimately you can see that the trend has picked up again and we are peaking at an all-time high, just as the stock markets are also peaking at fresh highs.

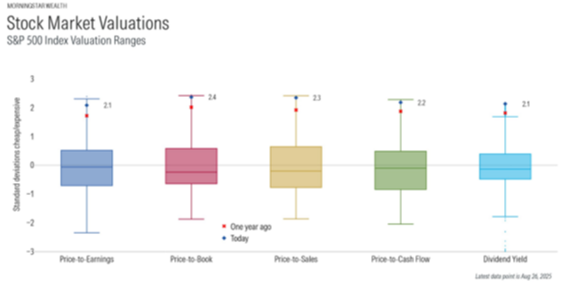

Much of this money out there in the system is being driven into stocks, driving the prices ever higher, ever more ridiculous.

No matter how you slice it—stocks are more than two deviations above the mean. This is another way of saying stock prices are 95% more expensive than they have been historically.

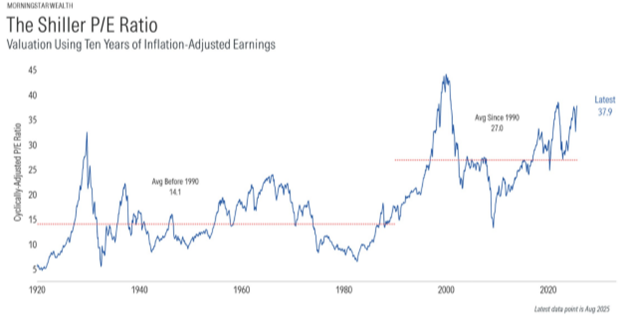

If recent history isn’t enough for you—let’s go all the way back to 1920—over 100 years. Here is what’s called the CAPE, cyclically adjusted price earnings ratio, which means it is adjusted for inflation. There were only two other periods when the CAPE was this high—the last time it was the Dot.com bubble in 2000, and the time before that—1929 and the Great Depression!

I’m not saying that we’re headed for another great depression, but I am saying that there are many reasons to be cautious and concerned. Cautious about another recession; concerned about more inflation to come.

The clear signs from our leaders in Washington are that inflation is the way, and the Big Beautiful Bill is going to lead to a big, beautiful bankruptcy. We are, de facto, already essentially bankrupt—economists call it “soft default.” As Professor Mises explained decades ago, “the advocates of public control cannot do without inflation. They need it in order to finance their policy of reckless spending and of lavishly subsidizing and bribing the voters.”

And here’s the thing—no one has enough money to buy all the debt that we’re spending, so the Fed has to buy it. But they buy it with money that they just create. This—in very real terms—reduces the value of the dollars in your pocket. Mises, right again: “The assistance of inflation is invoked whenever a government is unwilling to increase taxation or unable to raise a loan; that is the truth of the matter.”

We are unable to raise any more loans. This is why the bond yields are not dropping; this is why bond prices are not booming. It could be that we have truly maxed out our credit cards.

I know I harp on this incessantly—but it is because inflation attacks the most vulnerable in our society: the poor, pensioners, the uneducated, and the underemployed. I know that is not you, but you can see how stressed out everyone is. This leads to violence and lawlessness. Members of our youth feel helpless and hopeless.

The average age of a first-time homebuyer now is 38—because home prices have soared beyond attainability. Rent is roughly 40-50% of many people’s income, and as some have said recently, the stock market is not the economy. Stocks at all time highs can be attributed to all the cash that has been injected, but main street America is suffering from inflation, especially our younger generations. Once you see it, you can’t unsee it.

The Fed has said that they expect two more rate cuts this year, which will bring us down to 3.5%. So far, the bond market is not celebrating. In fact, it doesn’t seem all that happy about it (down about 1%), and it normally would be partying like it was 1999. But at least it’s not throwing a tantrum like it did last year.

It’s not completely clear what the Fed is trying to accomplish—other than maybe appease Trump—but lowering rates, increasing spending, increasing debt—is exactly what we don’t need. Professor Mises has a lot more quotes that will likely fit the situation we’re heading into, but let’s hope we don’t have to pull them out anytime soon.

As always, I would love to hear from you. Any comments, questions or suggestions are always welcome. Please contact me at kevin@magellanplanning.com if I can help in any way. Enjoy your Fall, and I hope to see you at one of our upcoming events.

Very Truly Yours,

J. Kevin Meaders, J.D. CFP, ChFC, CLU

The views and opinions are those of J. Kevin Meaders, J.D., CFP®, ChFC, CLU and should not be construed as individual investment advice, nor the opinions/views of Cetera Advisor Networks. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Additional risks are associated with international investing such as, currency fluctuation, political and economic stability, and differences in accounting standards. Due to volatility within the markets mentioned, options are subject to change without notice. The return and principal value of bonds fluctuate with changes in market conditions. If bonds are not held to maturity, they may be worth more or less than their original value.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of the 500 stocks representing all major industries.

Securities and advisory services are offered through Cetera Advisor Networks LLC, member FINRA/SIPC, a broker-dealer and registered investment adviser. Cetera is under separate ownership from any other named entity. Estate services offered by Magellan Legal, LLC and tax services offered by Magellan Tax, LLC. Estate and tax services offered separately from Cetera Advisor Networks LLC, which does not provide legal or tax advice.